Properly Structured Whole Life Insurance, Your Guide

When looking for an overfunded life insurance policy. It’s important to know that you have opted for a Properly Structured Whole Life Insurance policy.

There are 5 simple ways to spot a Properly Structured Whole Life Insurance product

- It should contain a Paid up Additions Rider

- There should always be a Term Rider

- It should have the right type of Term Rider

- It should have an increasing Death Benefit

- The first year cash value should never be zero

- The break even period should be between 5-10 years.

It Should Contain a Paid Up Additions Rider

Paid up additions are the life blood of an overfunded life insurance policy. It is the only way to infuse the life insurance policy with cash value quickly.

A life insurance policy is deemed paid up once all the premiums have been paid and the policy has matured. A paid up additions rider is simply a collection of smaller paid up policies to the base policy.

Let’s say you wanted to purchase $200 of life insurance. The insurance company might ask that you pay $100 for that policy. You still have access to that dollar, minus a premium fee. In this case we’ll use a 5% premium fee. This results in a $95 cash value.

Every year, the insurance company will credit you a dividend on that $95 cash value. Let’s say it’s 6% in this case. This is how your money would grow over a 10 year period

| Year 1 | $100.7 |

| Year 2 | $106.74 |

| Year 3 | $113.15 |

| Year 4 | $119.94 |

| Year 5 | $127,13 |

| Year 6 | $134.76 |

| Year 7 | $142.84 |

| Year 8 | $151.42 |

| Year 9 | $160.50 |

| Year 10 | $170.13 |

The problem is no one can just purchase a paid up life insurance policy directly from most companies. Even if you could, it would not be considered a life insurance policy in the eyes of the IRS. It is instead considered a Modified Endowment Contract.

It would be way too easy for people to put away cash in a life insurance policy as a tax shelter. By classifying a stand alone paid up insurance as MEC, some of the tax advantages of life insurance are no longer viable.

Though you can’t buy stand alone paid up policies, you are allowed to buy a standard life insurance policy, and add as much paid up life insurance as the insurance companies would allow. This is what we call a PAID UP ADDITIONS RIDER.

A properly structured life insurance policy will typically allow you to buy as much paid up additions as you can buy without the policy being deemed a MEC.

Term Rider is the “Cheat Code” of a Whole Life Policy

When properly structuring a whole life insurance for cash value, a term rider is always needed. As we mentioned earlier, there is a point where the paid up additions will turn your life insurance into a Modified Endowment Contract.

One of the reasons a policy becomes a MEC is when the cash value policy has exceeded the maximum limit to purchase a given death benefit.

One way to circumvent this problem is to add more death benefit at a low cost. As you already know, term life insurance is the most cost efficient way to add more death benefit to a policy.

Since the term rider adds more death benefit to your policy, your cash value is allowed to increase up to whatever the life insurance carrier would allow.

This is what separates a standard participating life insurance policy vs a properly structured whole life policy. There are plenty of insurance carriers who have paid up additions rider but not every one of them has a product that allows you to optimize the policy with a term insurance rider.

It Should Have the Right Type of Term Rider

Not all types of Term Riders are created equal. Most term riders added to Life Insurance policies are just an added temporary death benefit. However if the goal is to maximize cash value, the purpose of the term rider should be the same

It should be a slowly decreasing Term Rider as the Paid up additions increase.

The best life insurance products for cash value all have a Term Rider tied to the paid up additions (PUA) . As the death benefit of the PUA add up over time, it will slowly replace the term rider.

These term riders have a variety of names depending on the carrier. Here are some examples

- ALIR

- Enhanced PUA Rider

We all know that term insurance get really expensive as you age, it would be unwise to keep a term rider during the later stages of life. This is why it’s important for the PUA to replace the term portion of the policy.

It should not have a definite expiration date

10, 20 & 30 year Term Life insurance policies are great if death benefit is your objective. However, for cash value policies, you should stay away from any of these policies.

Remember that the purpose of the term rider is to increase death benefit to allow more cash into the policy. If it weren’t for the rider, your policy would be considered a MEC. If you have a policy with an expiring term rider, your policy would automatically become a MEC once it expires.

We have seen these products out there. We do know that there are agents out there selling these policies for cash value. Our stance on it is that you should definitely stay away.

It Should Have an Increasing Death Benefit

On a properly structured life insurance policy, the death benefit should always be increasing. As long as PUAs are being added to the policy, the death benefit should continue to grow.

On a standard policy, you typically buy a set death benefit. Your premium stays consistent and so does your death benefit. On an overfunded policy however, the premium is constant but the PUA and term rider should cause the death benefit to increase.

This feature makes a cash value policy very versatile. Though cash value is the main objective, an unintended benefit is the higher death benefit in the later years.

For someone who wants to also use these policies for death benefit, they should combine them with a term policy.

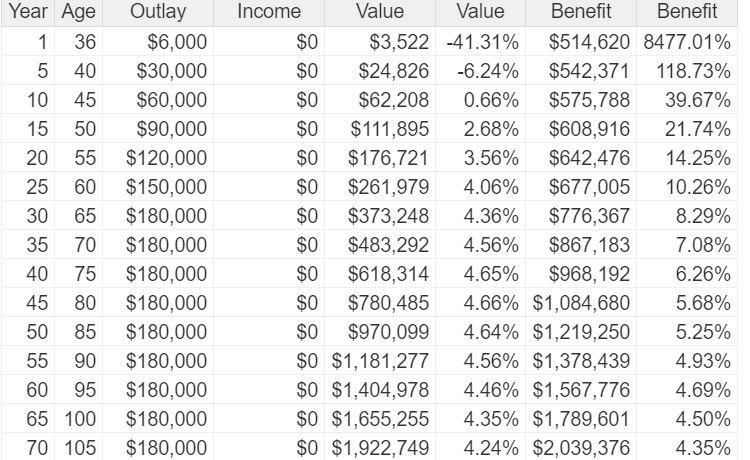

Here is how it works: Let’s say you’re 35 and paying $500/month for a $500,000 whole life policy for cash value. This cash value policy, while great for saving some long term cash, is not the most efficient way of getting a decent amount of death benefit.

This illustration and all others on this page are showing the non guaranteed columns. They assume the companies current dividend rates. These dividend rates may go up and down.

Let’s say you did want more death benefit. Instead of going for an inefficient whole life policy, the smarter play would be to get a term life insurance policy.

In our example, the death benefit is $514,000 at age 35 and slowly increases to over $700,000 by age 65. If you decided to buy an extra 30 year $500,000 term policy. You would have over $1M death benefit all the way up to age 65.

Although, the death benefits drops to a little over $700k after the term is over, it keeps increasing and achieves $1M by the time you reach 80. This is despite the fact that you have stopped paying premium at age 65.

Keep in mind age 65 to 80 is the period where most people would be spending down their retirement accounts. As you start to lose some of that cushion to pass down to the next generation, your death benefit keeps increasing. You won’t have to feel guilty about spending down the next generation’s inheritance.

It’s important to note that spending down the cash value of the policy also decreases this death benefit. This is a perfect case scenario if you’re either 1.) spending down a separate retirement account or 2.) only taking cash value out from time to time. This does not work if you’re using this policy for income distribution.

The First Year Cash Value Should Never be Zero

This is probably the simplest way for the average person to determine the efficiency of your whole life insurance policy. If you are unsure of a current policy illustration you have, check the first year cash value on both the guaranteed and non-guaranteed column. If it’s zero, you should question the design of the policy.

The Cash Value should be somewhere about 50-75% of the premium

If your first year cash value is somewhere around 30% there is a good chance that it’s somewhat properly designed. There is a chance this could be lower depending on your age.

At that point, it’s time to decide whether or not a cash value policy is ideal for your situation. At the later stages in life, the cash value policy is not efficient enough to grow because the death benefit becomes more expensive as you get closer to your life expectancy.

The Break Even Period Should be around 6-12 Years

If the first year cash value looks great on your policy, the next step is to look at the break even period. The break even period is when your total cash value has caught up to your cumulative premium.

Historically, this break even period has been closer to 5-8 years. However, due to a prolonged low interest rate environment, it’d be safer to assume 6-12 years and up to 12 depending on your current situation.

The reason for this slow growth is the front loaded cost of whole life policies. The first 2 years of the policy are where you pay the majority of the costs.

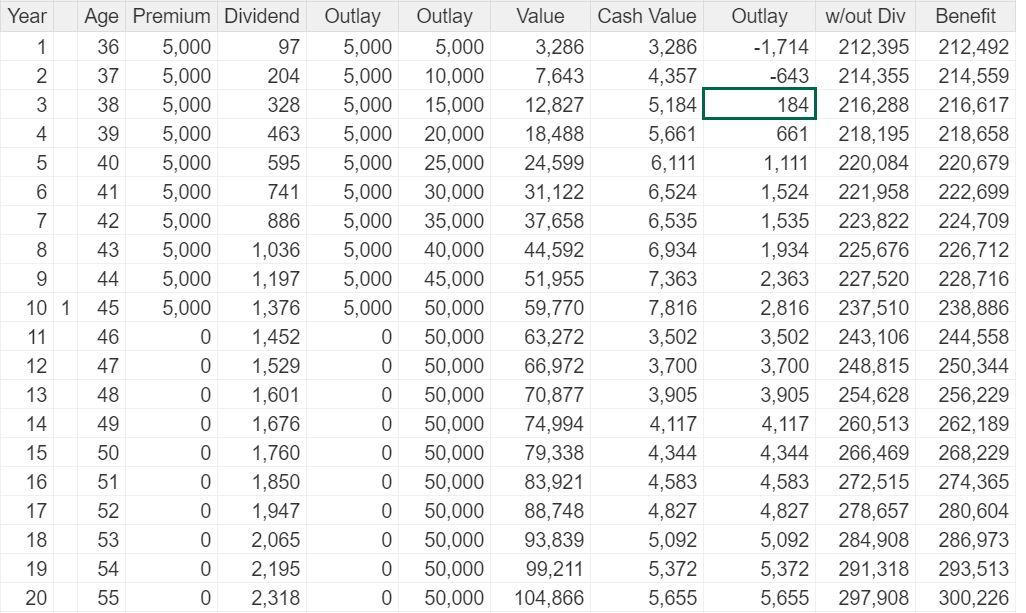

In this 10 pay policy above, you see that your $5000 premium turns into $3286 and $4357 in years 1 and 2 respectively. In year 3, it’s already positive at $5184.

However because of the lag in years 1 and 2 it takes 6 years for this policy to be positive. In year 6 after paying a total of $30,000 in premium, the policy is now worth $31122.

It’s important to note that these numbers are for this specific application. Your age and the pay period chosen are also a factor on how long it would take this policy to make it to the black.

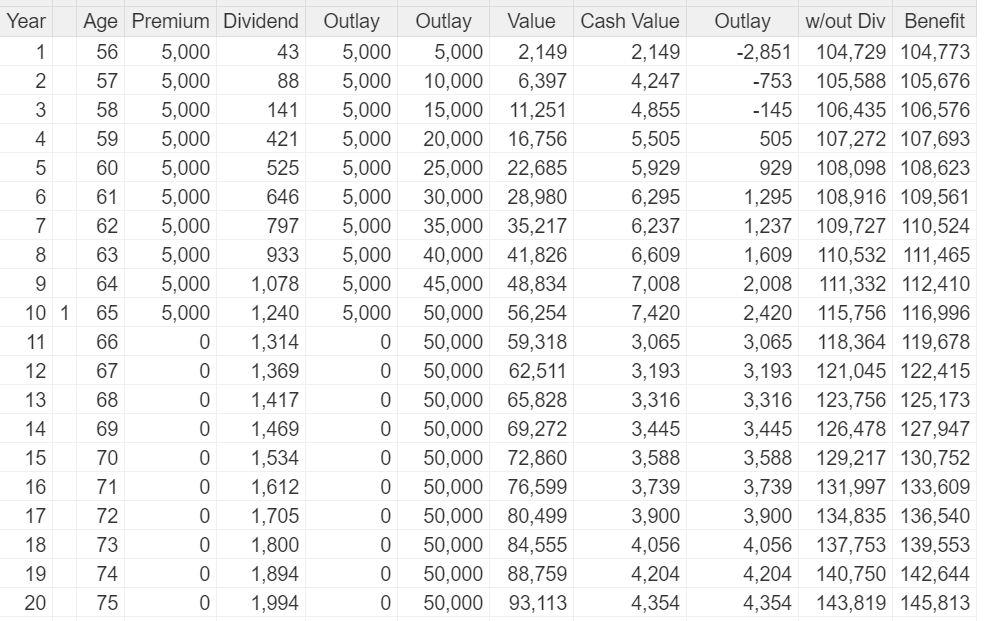

The example below is the exact same type of policy except for the age of the insured being 55.

What To Do If Your Policy Is Not Structured Properly

When the design of your cash value whole life insurance policy is not ideal, it may or may not be a good idea to cancel it. This depends on a few factors:

- The age of the policy

- The future outlook of the policy

- What you would want to accomplish with this policy

Age: The more mature the policy, the less likely you should cancel the policy.

As we mentioned earlier, whole life insurance policies are front loaded. If you have a 20 year old policy, chances is that you are way beyond the negative period of the policy.

If it’s a participating policy, it’s probably mature enough that it has earned a healthy dividend rate over that period of time. Also, because dividend rate were much higher 20 years ago, your policy reached a break even policy pretty quickly compared to today’s policies.

On the other hand, if you have a brand new policy, you might have more reason to cancel. The question to ask yourself is which policy will yield you the best return on your next premium payment.

If the newer policy comes out on top, then it’s a no brainer. If not, the newer policy might still win out in the longer term but that depends on what you’re trying to accomplish with this policy.

The longer your outlook, the more you should lean toward switching to the better policy.

Finding which year the newer policy wins out is critical in order to make a decision. If it’s not as clear cut as the 1st year, you have a decision to make.

Let’s say the newer policy starts to win out in year 10 and you plan to use the cash in year 15. You should ask yourself if it’s worth starting over to have to wait. Afterall, there is always a risk in starting over.

- Are you willing to wait 10 years?

- Will your situation be different 10 years from now?

- Is the extra cash you might earn worth the wait?

The answers to these questions are obviously a personal decision. We tend to be on the conservative side. A lot can change for an individual when we’re talking 5+ years down the line. Our stance tends to lean on keeping your old policy even if the 20 & 30 year numbers might look slightly better on paper.

Will you accomplish your goals with the current policy?

If this life insurance policy is part of a greater plan, you should ask yourself if you can execute the plan with this policy as it stands right now. If you can, you should probably lean toward keeping it.

A good example is someone who uses the cash value as a secondary emergency fund. A mature whole life policy may still yield a higher return than the alternative whether it’s properly structured or not. Starting over will still present a risk that may or not be worth it.